Exuberant markets are haunted by four ghosts

“Who you gonna call?”

Large cap US equities continued their strong run in May with the two-month return to 16.3%. That level of return places them in the top 0.5% of returns over the past 85 years, and possibly longer.

Whenever markets have run ‘hot’ it is wise to remind ourselves that while equities trend higher over the longer term, they are inherently cyclical, repeatedly rising above and falling below their long-term upwards trend.

Interspersed within this cyclical repetition are bear markets that reverse years’ worth of gains, often resetting short-term exuberance back to more fundamentally grounded levels, after which markets resume their long march upwards.

These patterns are fundamental to investing, and are the focus of much attention and research. Recently a number of papers have been published looking back at large historical market resets, focusing on financial shocks rather than exogenous ones like COVID.

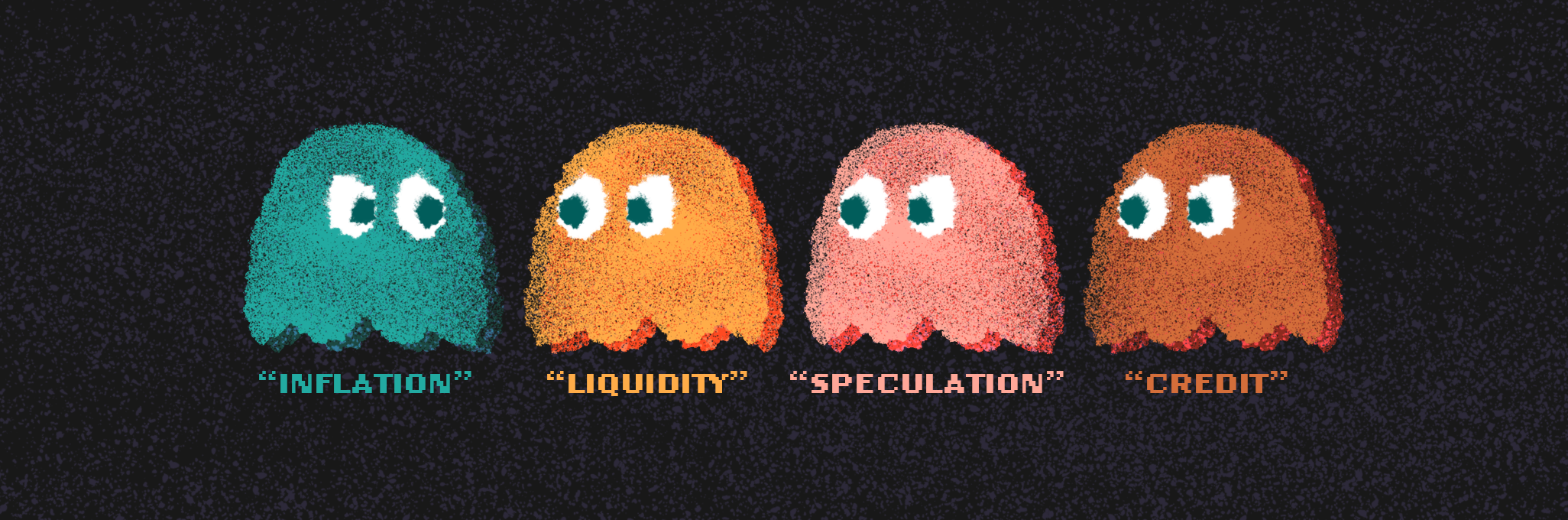

Bull markets don't die of old age, they're killed. Each of the great post-war drawdowns had a single, identifiable catalyst: inflation in 1973–74, a liquidity seizure in 1987, speculative excess in 1999–2000, and a credit crisis in 2008. We might comfort ourselves that these were separate, once-in-a-generation events.

Our uncomfortable premise is that the ghosts of all four conditions are looming simultaneously and, more troubling, they are now wired together.

Inflation: The ghost of 1974

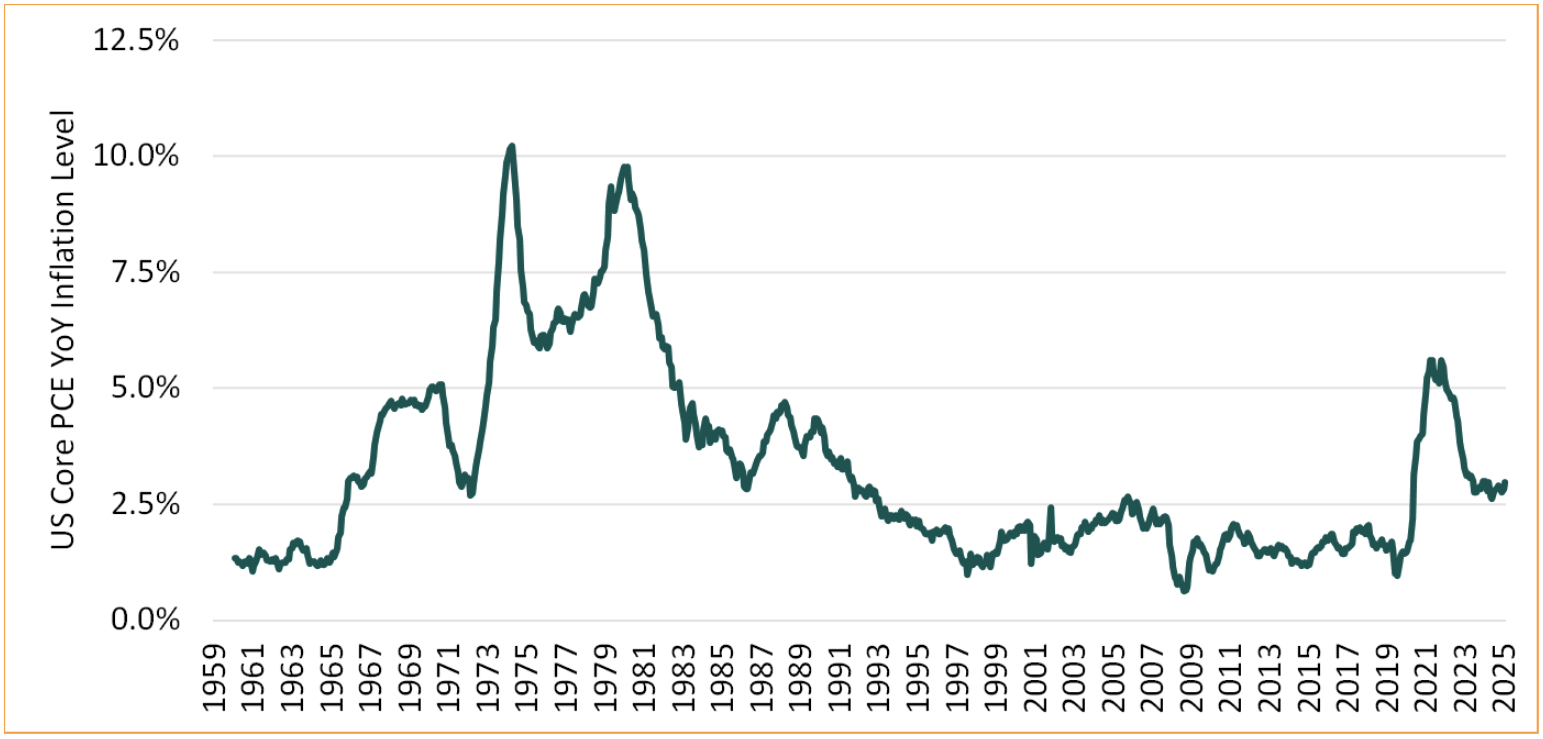

The 1973–74 bear market took roughly 48% off US equities, and far more in real inflation-adjusted terms. The catalyst was inflation marching toward 10%, driven by an oil shock and a Federal Reserve that was behind the curve. The damage, though, wasn't the inflation itself - it was multiple compression. Higher discount rates repriced every asset on the planet, and the long-duration darlings of the day, the "Nifty Fifty" trading at 50–90x earnings, de-rated hardest. The real warning in that chart is the double peak: inflation rolled over after 1974, policymakers eased, and a second, worse wave followed into 1980. Today, US Core PCE inflation has stalled near 3% rather than returning to target 2% and is again reaccelerating - the latest reading rose to 3.3% - against a fresh oil shock and commodity prices up around 40% year-on-year. The risk isn't that we failed to beat inflation. It's that we're writing the 1976 chapter: declaring victory one wave too early.

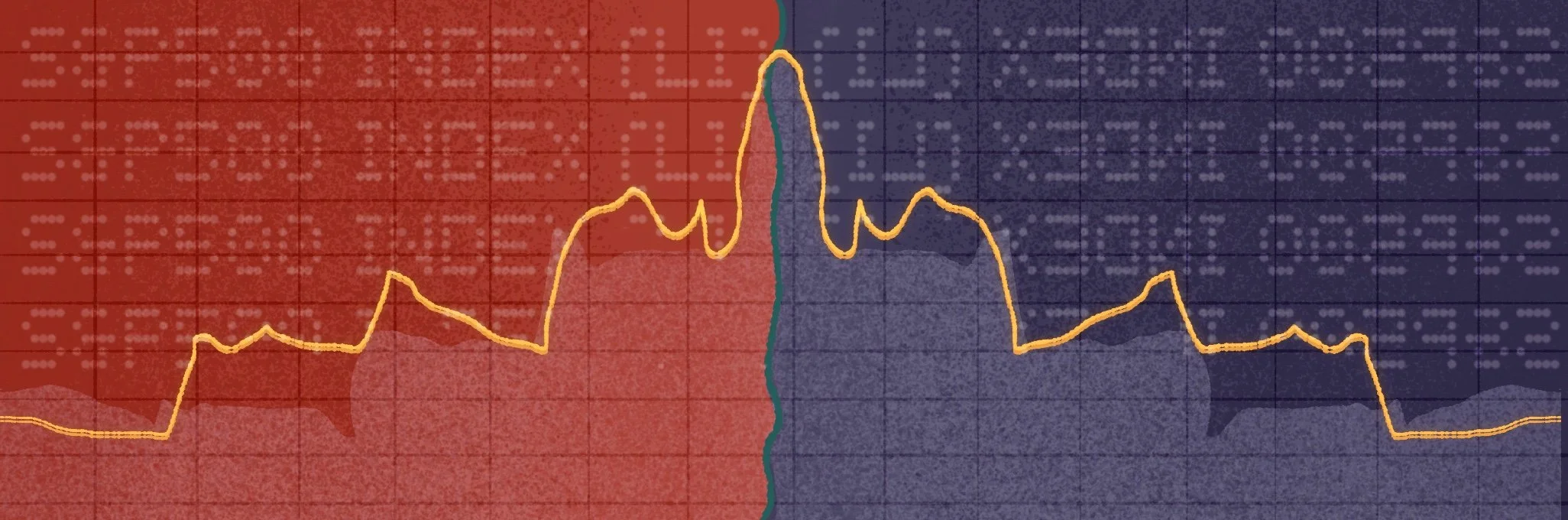

Figure 1. Select index drawdown, April bounce strength

Source: Bloomberg, Human Financial

Liquidity: The ghost of 1987

On 19 October 1987 the US equity market fell 22.6% in a single session with no fundamental trigger. A popular algorithmic hedging strategy, Portfolio Insurance - that sold automatically as prices fell - turned an ordinary decline into a cascade until liquidity simply vanished. The amplifier then was a sliver of total volume. Today, by indicative estimates, 60–75% of US equity volume is computer-driven, and zero-day options are close to half of all S&P 500 options flow. Volatility-targeting funds, trend-following CTAs, leveraged ETFs and dealer gamma hedging are effectively portfolio insurance at scale and speed.

And that failure mode keeps recurring:

The 2010 "Flash Crash" saw market-makers pull their quotes as one large futures sell order hit thin liquidity, briefly erasing nearly 9% from the Dow;

2018's "Volmageddon" blew up a crowded short-volatility trade as spiking volatility forced the inverse-VIX products to buy more of it;

March 2020's "dash for cash" froze even US Treasuries as leveraged investors de-levered at once; and

The August 2024 yen carry-trade unwind sent volatility to near-record highs before reversing within a week.

Different triggers, but an identical mechanism: price-insensitive selling overwhelming liquidity that vanished exactly when it was needed. And these have clustered in the past 15 years after decades of rarity. This ghost rarely strikes first, but it amplifies whichever one does.

Speculation: The ghost of 2000

The technology sector accelerated vertically into March 2000, then fell about 80%. The sector didn't reclaim its high for the better part of two decades. The internet was real, but equity prices weren't, and capital expenditure had run years ahead of monetisation. Today the concentration is, on several measures, worse than the dot-com peak: the ten largest stocks are around 41% of the S&P 500 versus roughly 27% in 2000, semiconductors have gone from about 2% to 18% of the index, a single chipmaker sits near a $5 trillion valuation, and more than $1.25 trillion has been committed to AI infrastructure in twelve months. The honest difference is that most of today's leaders have real earnings and lower multiples: the sector trades near 35x forward versus roughly 60x in 2000. But there are familiar echoes: in the adoption gap – only about a fifth of enterprises have actually deployed AI against equity values that assume far more; and in the circular financing – in which chipmakers fund their own customers just as vendor finance flattered demand in the late 1990s.

Credit: The ghost of 2008

2008 was a credit event that equities merely rode down: leverage and funding, not earnings, were the problem. The detail that should haunt every investor: through 2007 the recession models were already flashing while high-yield credit spreads sat at record lows. Spreads were the final indicator to move, gapping toward 20% only once the crisis was underway. Today high-yield spreads are around 2.75%, near the tightest on record and essentially back at their 2007 levels: investors are paid almost nothing to carry credit risk. And a great deal of leverage has migrated into private credit, off the public screen entirely. A tight spread today does not necessarily mean the risk isn't there; it may mean the risk has simply moved somewhere you can't see it.

A spectral convergence

Here is the spectre worth pondering. The ghosts aren't merely co-present - they're interlinked. The AI capex boom (speculation) is increasingly funded in credit markets at the tightest spreads in a generation (credit). Reaccelerating inflation threatens the very discount rate that justifies record equity concentration (inflation feeding speculation). And whatever shock lands first, market structure guarantees it is amplified mechanically while liquidity evaporates on the way down (liquidity multiplying all of it). In 1974, 1987, 2000 and 2008, the market faced one crisis at a time. The scenario we are quietly underwriting now is one where a single catalyst - an inflation surprise, a credit wobble, an AI capex air-pocket - is transmitted through all four channels simultaneously.

The honest counterweight

None of this is a forecast of imminent collapse, and we should resist the seduction of a tidy doomsday narrative. Each ghost has a credible rebuttal: today's Fed has far more inflation-fighting credibility than Arthur Burns'; the tech leaders generate real cash; the capex is (until recently) funded more from earnings than debt; and algorithms genuinely add liquidity in normal conditions. Bears have been wrong for years, and derisking early has carried an enormous opportunity cost. The point is not to predict the date. It is that the conditions for a major repricing are more completely assembled, and more tightly coupled, than at any time since at least 2007 - even as implied volatility, credit spreads and general complacency insist the opposite.

Who you gonna call? What it means for portfolios

We are not positioning for the apocalypse. We are positioning for fragility. That means treating liquidity as a risk factor in its own right, holding genuine diversifiers and dry powder, being disciplined about what we'll pay for concentration, and refusing to read a calm surface as a safe one. The four ghosts have haunted markets before - one at a time - and each time the warning looked obvious only in hindsight. The unusual feature of this moment is that all four are lurking at once. The question is no longer whether they strike. It's which one looms first, and how hard the others amplify the charge.

More like this