She’ll be right…won’t she?

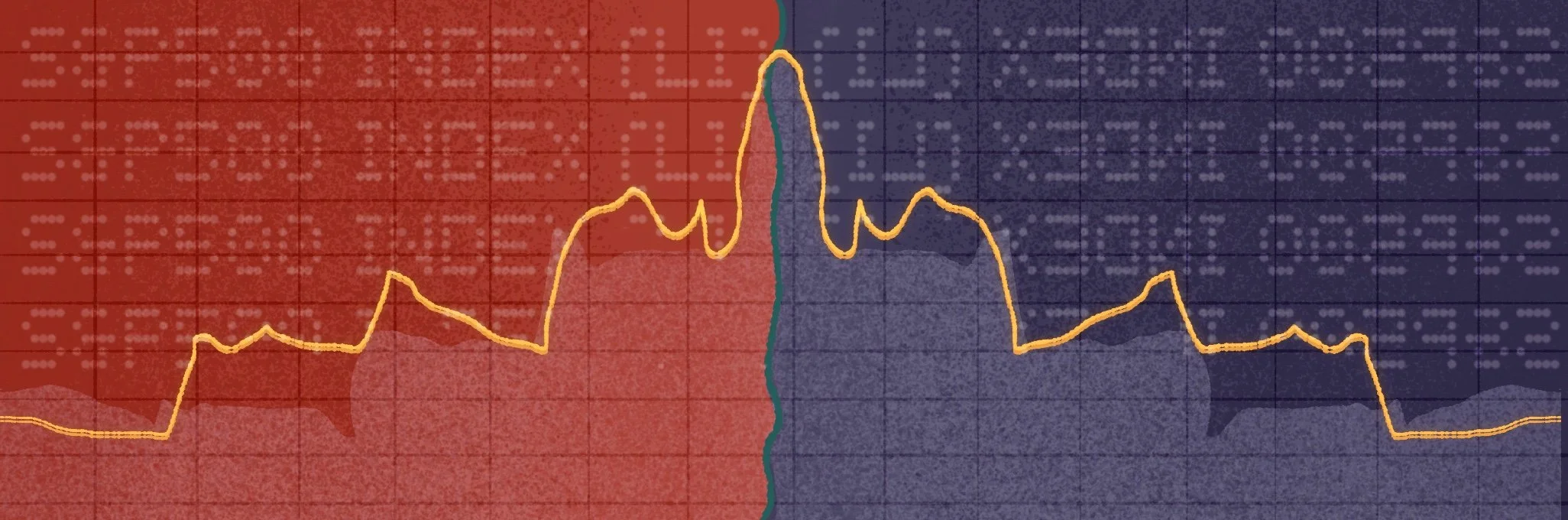

April 2026 was, by almost any historical measure, an extraordinary month for equity markets. Across most major indices, April returns ranked in the 1st or 2nd percentile of all monthly returns on record, some of the strongest single months in 30-plus years of market history. And yet, when set against the drawdowns that preceded them, those same returns left nearly every index still deeply in the red for the period.

The S&P 500, the best outcome in the table, finished the combined period barely positive at +0.4%. Everything else remained negative, in some cases dramatically so. The ASX 200 is perhaps the sharpest illustration: it suffered a Q1 drawdown identical to that of the S&P 500, at -9.1%, yet its April recovery ranked only in the 25th percentile against history, leaving it -7.1% for the combined period. Same starting loss, but a recovery 17 percentage points lower.

Figure 1. Select index drawdown, April bounce strength and cumulative performance

| Index | Q1 max drawdown |

April return | April return percentile* |

Drawdown + April bounce (compounded) |

|---|---|---|---|---|

| ASX 200 Technology Sector | -50.30% | 13.30% | 7% | -43.7% |

| ASX 200 Consumer Discretionary Sector | -27.60% | 1.30% | 36% | -26.7% |

| MSCI Australia Small Cap | -16.50% | 4.50% | 20% | -12.7% |

| ASX 200 | -9.10% | 2.20% | 25% | -7.1% |

| S&P 500 Consumer Discretionary Sector | -16.10% | 11.73% | 2% | -6.3% |

| S&P 500 Technology Sector | -18.40% | 17.50% | 1% | -4.1% |

| Emerging Markets (in AUD) | -10.80% | 9.30% | 2% | -2.5% |

| MSCI World Growth | -12.80% | 12.30% | 1% | -2.1% |

| MSCI World Small Cap | -8.70% | 7.50% | 6% | -1.9% |

| MSCI World Value | -7.60% | 7.10% | 7% | -1.0% |

| MSCI World | -8.90% | 9.60% | 2% | -0.2% |

| S&P 500 | -9.10% | 10.50% | 1% | 0.4% |

Source: Bloomberg, Human Financial, as at 30th April 2026. *Ranked monthly return against index's own history over past 30 years or since inception.

That is the central paradox this period illustrates: you cannot have the recovery without first absorbing the drawdown. The two are not separable. An investor who avoided the Q1 pain avoided the April bounce in roughly equal measure. An investor who held through the drawdown earned the recovery, but in most cases, not enough of it to get back to even.

The pattern across the table is consistent. In general, the deeper the Q1 drawdown, the stronger the April return, yet the net result remains negative in almost every case. ASX 200 Technology is the starkest example: a 50.3% drawdown followed by what would ordinarily be considered an exceptional +13.3% April, yet the combined position is still -43.7%. The mathematics of loss recovery are unforgiving; halving a portfolio requires a 100% gain to restore it. A record month doesn't change that arithmetic.

The more important observation, however, is not the arithmetic, it is what markets appear to be telling us about risk. And right now, markets appear to be telling us: she'll be right…

"She'll be right" is a uniquely Australian expression and not merely a casual one. It carries within it a distinct cultural philosophy: a relaxed fatalism, born from generations of making do in a landscape that doesn't always cooperate. The expectation that things have a way of working themselves out if you don't overthink them. It is stoicism with a suntan. At its best it is a genuine psychological asset, the ability to stay calm, absorb a shock, and keep moving. The British equivalent, forged in a rather different climate, was "Keep Calm and Carry On", a wartime instruction that has since become something of a global export. Both share the same essential message: don't panic, trust the situation to resolve. Both are admirable in the right circumstances. And both, applied uncritically to investment risk, can be quietly catastrophic.

Embedded in April's extraordinary returns,and most pronounced in the US, are two assumptions, each optimistic in its own right. Taken together, they form a worldview that we think deserves serious scrutiny. The first is that the risks are fading, the Middle East conflict will resolve, oil will retreat, inflation will ease and the macro environment will normalise. The second is that the positives will not merely persist but accelerate: that earnings growth, AI-driven productivity and consumer resilience will continue to compound in the months ahead.

April priced both assumptions simultaneously. We are less convinced that either is assured, let alone both.

Australian equities in April told a an optimistic, yet different story. They ranked in the 25th percentile of their historical monthly returns, meaningful but behind the global experience. That gap reflects Australia's structurally different exposure to this kind of shock. Unlike the US, Australia is not energy independent, and geographically we sit at the bottom of the world, a great place to be when rockets are flying in the northern hemisphere, but also literally at the end of almost every global supply chain. With that comes additional cost and complexity, leaving us a price taker on almost every major import. The result is a more sober local assessment of persistent inflation, a hawkish RBA, and the ongoing sensitivity of domestic earnings to sustained energy costs. In short, Australian markets are not yet convinced it will all be right, and we think that scepticism is warranted.

The geopolitical shock that drove Q1 drawdowns has not been resolved. It hasn't even paused.But it is being ignored. Oil remains well above $100 a barrel, the Strait of Hormuz has not normalised, and inflation expectations in both Australia and the US are moving in the wrong direction. The faith that risks are subsiding and that the good times are accelerating may yet prove well-placed. And the rallies were real. The historical significance of April's returns is not in dispute.

But when some of the strongest monthly returns ever recorded leave nearly every index still negative for the period, it is worth asking what a genuine resolution, or a genuine deterioration would look like by comparison. In our view, the risk premium embedded in current prices does not adequately reflect the range of outcomes. “She'll be right” is a disposition, not a risk management framework. “Keep calm and carry on”, while excellent advice for the Blitz, was never intended as a portfolio management tool.

From Human Financial’s perspective, we continue to manage money the way we always have.

Right now, that means maintaining a higher level of diversification and the defensiveness that it brings. In our Dynamic models we remain underweight growth exposures and will likely increase this underweight if markets continue their risk-ignorant rally. Where we were hedging AUD in our global growth exposures, we have reduced these currency hedges significantly, which should further increase our downside protection. That combination of patience and disciplined risk management has served our clients well over the past six months and remains the foundation of our long-term approach.

More like this