Markets enter a curious and ambiguous phase

September monthly commentary

Markets have entered a phase in which fundamentals and sentiment seem increasingly disconnected. Any professional investor with a risk-management mindset is likely to be trimming exposures or sitting on the sidelines; while other investors continue to shoot for the moon. The backdrop is ambiguous at best: strong price action and speculative enthusiasm suggest confidence, while positioning and caution among institutional investors imply unease.

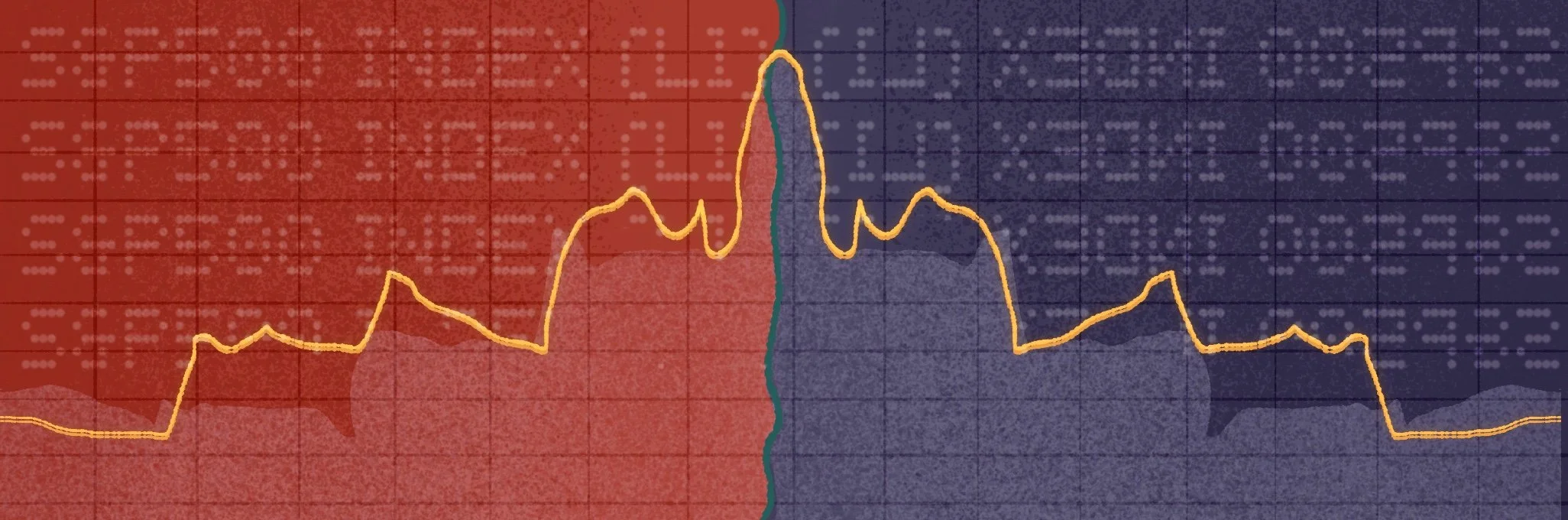

Adding to this sense of tension, Buffett’s U.S. market cap-to-GDP ratio—a broad gauge of overall equity market valuation—has reaccelerated to historic new highs. This measure, often dubbed the “Buffett Indicator,” underscores how far asset prices have run ahead of underlying economic output. It reinforces the notion that optimism may be pricing in perfection, leaving little margin for error if growth or earnings disappoint.

Buffett’s U.S. market cap-to-GDP ratio: Back to record highs

Source: Human Financial, Bloomberg

Complicating matters, the current US government shutdown will have markets flying blind on data for the near future. Even once this ends, it will take time for workers to return, clear the backlog, and resume publishing economic reports. In the meantime, investors are likely to discount any short-term negative data as distortion from the shutdown rather than evidence of a genuine slowdown. That, in turn, may sustain the sense of complacency for a while longer.

The bigger question is whether this is simply a cyclical upswing within the market’s long-term structural grind higher, or the makings of a bubble, as some fear. The outcomes appear increasingly binary: to the winner go the spoils. If the AI-driven productivity story delivers, the long-term payoff could be enormous. Yet history reminds us that every transformative technology endures a “trough of disillusionment”, when early exuberance fades before steady progress resumes.

Could AI face that reckoning in the years ahead? Or will the vast ecosystem of spending, innovation and optimism prove resilient enough to power through? Either way, markets today are balancing exuberance and exhaustion in equal measure - a mix that makes prudence feel as contrarian as it is sensible.

Amid this, our consistent identification of an economic regime change remains intact. We believe the global economy is transitioning toward a stagflationary scenario, characterised by persistently higher inflation and slower growth. Historically, that has been one of the toughest environments for asset returns, as both equities and bonds struggle to deliver consistent real gains.

When uncertainty is elevated, valuations are stretched, and the macro regime itself is shifting, our view is that the best course of action is to discount conviction and temper enthusiasm. Confidence can be costly when clarity is lacking. To invest through such an environment, we continue to rely on diversification and maintain a cautious asset allocation stance: seeking to participate where the risk/reward justifies it, while preserving flexibility for whatever comes next.

More like this